Sector Background and Potential

The Philippines is significantly underinvesting in physical infrastructure, with its public sector infrastructure budget consistently below 3% of GDP. Spending on social infrastructure for education and health is also inadequate at slightly over 4% of GDP.53

Polls of businessmen repeatedly show poor infrastructure as one of the top challenges facing the Philippine economy, second only to corruption. Like corruption, poor infrastructure severely weakens economic competitiveness.

In the last two WEF Global Competitiveness Reports, among the ASEAN-6 economies, the country’s overall infrastructure quality ranked below Singapore, Malaysia, and Thailand and about the same as Indonesia and Vietnam (see Figure 65).

____________

53 Based on calculations from the Asian Development Bank (ADB), as percentage of GDP, the Philippines spent about 2.9% on education, 1.2% on social security, 0.5% on health, and 0.1% on housing and community amenities in 2008. The 2009 DepEd budget of PhP 158 billion represents a per student spending of PhP 8,000 for each of the more than 20 million students in basic education, one of the lowest spending levels in Asia.

|

|

Table 27 shows a similar pattern of the Philippines in comparison to the ASEAN-6 countries for measures of power quality, telecommunications, access to water and sanitation, and roads. The Philippines is ranked the lowest for fixed telephone lines per 100 inhabitants and percentage of total road network paved.54

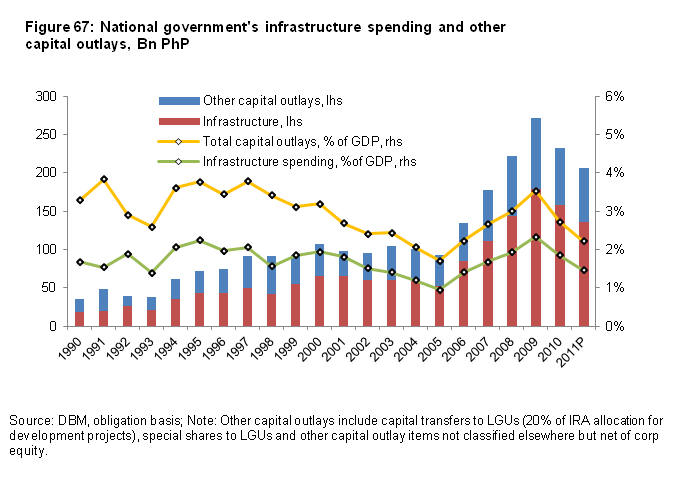

The Philippines spends a lower percentage of GDP on infrastructure than competing ASEAN economies, as shown in Figure 66. After reaching a low of 1% in 2005, the percentage increased to 2.1% of GDP in 2009 (see Figure 67). If spending on infrastructure continues to remain low, efficient modern infrastructure will not be built fast enough to meet the challenge of being an archipelago with a high and rising urban population density.

Figure 66: Infrastructure spending, ASEAN-5, % GDP, 1980-2009 (annual average)

_____________

54 While 70% of the national roads are paved, only 14% of the local roads, which comprise 85% of the total road network, are made of concrete or asphalt.

|

|

Figure 67: NG Infrastructure spending, Philippines, 1990-2009

View updated figure here

Inadequate funding for infrastructure during the last decade contributed to the weakened competitiveness ratings for the country’s overall infrastructure as well as the continued listing of poor infrastructure as a major weakness in its investment climate. Despite the availability of external private and public sector financing, the government was unable to implement significant Public Private Partnership (PPP) projects nor could it avail of significant sums of low-interest loans for infrastructure from China. A lack of transparency and extraordinary levels of public controversy characterized what in most countries is routine infrastructure project development and implementation.

The administration of former President Macapagal-Arroyo in 2003 began a policy initiative to improve inter-island connectivity through the RORO Road Terminal System (RRTS). In her 2006 SONA former President Macapagal-Arroyo highlighted more than 400 projects (mostly related to air, ground, and marine transport) targeted for completion before the end of her term in 2010.55 Some of the projects were criticized as politically motivated to dissuade congressmen from supporting an impeachment motion against the president.

The overall infrastructure record of the outgoing administration is weak, considering it had almost ten years to complete projects. It neglected to start many major projects and to utilize several which were completed. The administration expropriated the privately-owned international passenger terminal at the national gateway airport in December 2004. The Philippine-German joint venture that built the terminal has not been compensated after more than five years, despite the assurances of the Philippine government that all issues would be settled expeditiously. There are new ports in Batangas and Subic which are hardly used. The Department of Transportation took seven years to approve a US$ 1 billion light rail project in Metro Manila. For ten years it was unable to decide how to bid and award another large light rail project. Manila residents paid a terrible price in lives and property when one typhoon’s torrential rains proved the high risk of neglecting flood control infrastructure and unregulated urban sprawl. Maritime safety remains a major issue, highlighted by many small and several large disasters. Power blackouts became frequent in the Visayas and Mindanao in 2010.

_____________

55 Subsequently, the president issued several executive orders creating an Infrastructure Monitoring Task Force to oversee implementation of the projects and then renaming the Task Force as the Pro-Performance System Steering Committee and adding private sector representatives. The Presidential Management Staff serves as secretariat.

|

|

The Philippines faces urgent infrastructure challenges. The most urgent is assuring an adequate supply of power, eventually reducing its cost through increased competition among generators. The second is improving the efficiency of transportation, by air, land, and sea, which is too crowded for a population growing in size and spending power. A third is the water supply, which is not enough for drinking and farming and too much during typhoon season, as well as poor sanitation and solid waste disposal systems. By contrast, telecommunications services, in the hands of competing private sector providers, are much improved following reforms initiated by President Ramos in the 1990s.

The three following tables list major infrastructure projects of both the public and private sectors. The projects in each are listed by category as airport, power, rail, road, seaport, telecommunication, and water. The tables cover three different time periods, with the later including several projects still at the conceptual stage.56

• Table 28: Completed projects (2001-2010)

• Table 29: Under construction or being financed in 2010

• Table 30: Priority future projects (2011-2020)

Table 28: Major infrastructure projects completed, 2001-2010

__________________

56 Sources for the three tables vary but include media reports and government websites, data from the Pro-Performance System Steering Committee secretariat and industry experts. Project costs are approximated in dollar terms and may not reflect actual peso costs because of exchange rate conversion variations.

57 Expropriated by the Philippine Government in 2004; the final amount of compensation due to the German-Filipino joint venture owner ($64 million has been paid) has been undergoing arbitration at the International Chamber of Commerce International Court of Arbitration in Singapore for several years, with final approval to be made by a Philippine court.

|

|

Table 29: Major infrastructure projects underway,58 2010

_____________

58 Underway includes projects undergoing financing and under construction.

|

|

Table 30: Major infrastructure projects to implement, 2011-2020

___________________

59 Any policy to declare Coron and Puerto Princesa as pocket open skies airports should include upgrading each airport’s infrastructure to international standards including international flight rules (IFR) capabilities.

60 Unsolicited bids have been submitted.

61 Power generation cost estimates assume US$ 1 million per MW for coal and gas, US$ 2 million for hydro and wind, US$ 2.4 for biomass, and US$ 2.5 million for geothermal and nuclear.

62 Provincial bus operations to and from the North and South could start and terminate at these bus terminals. The light rail system will provide inter-modal connectivity to and from the metropolis.

|

|

Arangkada Philippines 2010 does not analyze or make recommendations for the entire infrastructure of the Philippines.65 This policy paper focuses on major projects in Central Luzon and the NCR, where most of the country’s industry is concentrated and where one of the world’s largest urban mega-regions is rapidly expanding (see Table 31). Manila presently is the world’s 5th largest urban area with an estimated population of 20.8 million in 2010. By 2030 Manila is projected to be the world’s 3rd largest urban area (after Jakarta and Tokyo-Yokohama) with a projected population of 34 million inhabitants. An increase of 13 million residents will require very large investments, not just to maintain the current poor condition of infrastructure but to achieve substantial modernization to improve national competitiveness.

___________________

63 US$ 190 million for Phase 1 6-lanes Quezon City to Baliuag, Bulacan; subsequent phases will traverse Nueva Ecija north to Tuguegarao, Cagayan.

64 Arangkada Philippines 2010 recommends a policy to decongest Manila Port by gradually shifting international container traffic to the ports of Batangas and Subic to utilize the completed facilities at both ports for international container shipping.

65 The World Bank’s extensive 2005 study “Philippines: Meeting Infrastructure Challenges” contains data and recommendations still valid. More recently, the Philippines-Australia Partnership for Economic Governance Reforms (PEGR) prepared the Draft National Transport Policy Framework document dated October 30, 2009.

|

|

Table 31: Population of Urban Mega-regions, 2010 and 2030 (E)

Many of the recommendations made for the Seven Big Winner sectors require infrastructure in the country’s other urban centers and rural areas. The Agribusiness sector needs better farm-to-market roads and post-harvest facilities, including cold chain storage, and ports. Mining require better roads and ports. Interisland shipping needs to be safer, more efficient, and less costly. Most of the country’s most attractive tourist destinations need better air and sea access, improved roads, water, and sanitation. Increasing business processing investment at secondary and tertiary cities requires dependable telecommunication links, while reliable and lower-priced power is essential for the entire economy.

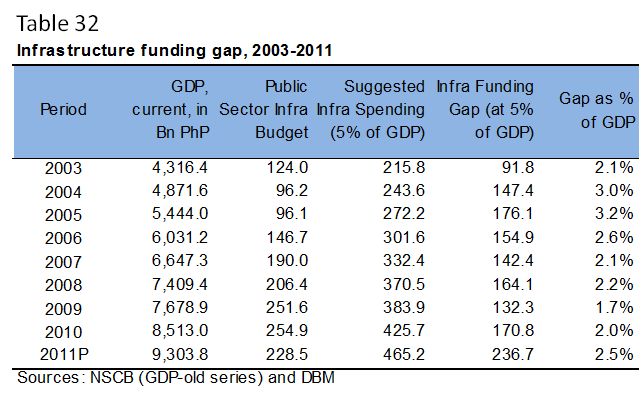

Turning this vision into reality in a decade can be possible if recommendations in the following sections are implemented. Funding in the tens of – perhaps as high as one hundred – billions of dollars will be needed (see Table 32). Such large amounts of funding are not available from the public sector and ODA, but can be provided by the private sector, both domestic and foreign, investing in PPPs. However, private investors will only participate in well-prepared projects in an investment climate that provides them contractual and regulatory confidence of fair returns on their equity.

|

|

Table 32: Infrastructure funding gap (Bn PhP), 2003-2010

View updated figure here

In the following pages, Arangkada Philippines 2010 presents recommendations developed at three FGDs on infrastructure hosted by the American Chamber of Commerce: (1) Airports and Seaports, (2) Power and Water, and (3) Road and Rail. With some exceptions, recommendations focus on the geographic area from Batangas north to La Union province, an area with a population of over 36 million and the highest PCI in the country at about US$ 2,468.66

___________

66 Per capita income is computed using the 2008 Regional Gross Domestic Product (RGDP) of NCR and regions 1-4 divided by the 2008 population estimates of NSO covering the said regions. 2008 RGDP data are the latest figures available. The average exchange rate in 2008 which is PhP 44.4746 per US$ (BSP) was used to convert the value in current dollar terms. Total population of the area was computed by simply summing up the 2010 population estimates of NSO for the provinces of La Union, N. Vizcaya, Quirino, Pangasinan, Tarlac, N. Ecija, Aurora, Zambales, Pampanga, Bulacan , Bataan, NCR, Rizal, Cavite, Laguna, and Batangas.

|

|

Reforming the Infrastructure Policy Environment

Legal issues

• Build-Operate-Transfer (BOT) Law

The BOT Law (RA 6957), enacted in 1990 and amended in 1994 (RA 7718), is the legal framework for BOT and PPP projects. However, there is no single government agency in charge of BOT/PPP planning and project preparation, and very little is said in the law about the role of the government for project planning and preparation, principles and policies on risk sharing, and risk allocation.

• Unsolicited Proposals

Too many contracts are awarded under the unsolicited mode. RA 7718 states that the government may accept unsolicited proposals provided that the project involves a new concept or technology, requires no government funding, and/or is not part of the list of priority projects. Projects have been removed from the priority list to qualify for unsolicited proposals. The timeframe for developing a proposal under Swiss challenge (i.e. 30 days) is too short.

• Joint Venture Agreements (JVA)

The head of a government agency has full authority to sign a JVA. This process lacks transparency and competition. The public becomes aware of the project only after the agreement is done, and terms of the agreement are not usually disclosed. Other government agencies (e.g. DBM, DOF) learn of the project only when funds need to be released. NEDA has no oversight role in the approval process. The JVA has become a preferred mode of private sector participation in infrastructure projects, as the approval process is significantly shortened, and oversight is almost nonexistent.

• Foreign Equity Restrictions

In the Government Procurement Reform Act (RA 9184), a 25% cap on foreign equity is imposed on some infrastructure projects. In some projects where security is an issue, foreign equity is reduced to zero. Some projects require advanced technologies that may not be locally available. Foreign companies can provide such technologies but their participation is limited and opportunities to partner with local companies are limited.

Project Planning, Prioritization, and Approval

• Long Term Planning

There is lack of long-term planning for infrastructure development. Usually, project duration is co-terminus with the term of an administration. New projects that cannot be completed towards the end of a presidential term are no longer implemented nor prioritized.

• Lack of Technical Capability to Plan and Prepare BOT Projects

The government has not demonstrated the technical capacity to plan and prepare documents for potential BOT and PPP projects. As a result, many projects encounter problems that delay implementation and sometimes lead to cancellation.

The government must have the capacity to determine which projects are commercially viable for the private sector. At present, there is a BOT office in the DTI, but it has very limited staff and inadequate technical capabilities and financial resources. Project preparation requires technical expertise, commitment, and an adequate budget for the preparation of feasibility studies, bid terms of reference, etc.

___________

67 Of the three FGDs devoted to infrastructure, the Road and Rail FGD spent considerable time discussing more general infrastructure policy issues applicable to most sectors. The recommendations are included here and the discussion specific to road and rail projects appears after the section on “Power.”

|

|

The role of government is not limited to preparing the list of priority projects but extends to the preparation of necessary documents to make the BOT process work. For example, government hastily identified the Panguil Bay Bridge project in Mindanao for BOT financing without the benefit of a feasibility study. Three years later, the Department of Public Works and Highways (DPWH) determined it was not commercially viable for the private sector.

Senior government officials present brochures and power point presentations in meetings and conferences showing Potemkin-like projects “offered” to the private sector.68 When the private sector enquires about their details, including bidding schedules, answers are evasive.69 However, when projects are viable and well-prepared and the process is transparent, investors and lenders will come in (see “Transparency in Procurement and Implementation” below).

• Politicized Project Prioritization

The Office of the President has great discretionary power regarding the release of Countrywide Development Funds (CDF), which are often used to reward political support. A study shows that only 38% of CDF infrastructure projects came from Highway Development and Management Version 4 (HDM-4) generated projects.70 Most (62%) are politically determined. HDM-4 is a framework that allows for the systematic prioritization of infrastructure projects. The CDF originated after the 1987 elections with an allocation of one million pesos per representative and has increased to PhP 70 million. Each senator is allocated PhP 200 million. These amounts are usually budgeted annually.

Slow Project Approval

Infrastructure project approval in the Philippines is very slow. Investors have to wait a minimum of five years before a project is approved. Immense time and effort are needed from the start of the planning stage to approval. Inefficiency adds to project expenditure, raising the cost of doing business and the cost of the project itself. To prove that the GRP is serious in improving infrastructure, there is a need for a faster, yet still reliable, project approval process.

Infrastructure Budget and Release

• Congress re-allocates the DPWH budget

Congress inserts, deletes, and realigns some of the projects submitted under the president’s National Expenditure Proposal submitted to Congress each year. The list of approved projects in the General Appropriations Act (GAA) usually differs from the NEP. However, OP-DBM may impound the appropriated budget for some projects (listed in the GAA) and realigned to other projects (proposed by political allies).

_____________

68 Potemkin refers to a pretentiously showy or imposing fa硤e intended to mask or divert attention from an embarrassing or shabby fact or condition (Random House Unabridged Dictionary, 1997).

69 The former Secretary of Finance and the former Acting Director General of NEDA presented projects at the April 2008 Philippine Development Forum (PDF) at Clark. The same projects were presented at the Wallace Business Forum in Makati by the DTI Secretary in December 2008. At both fora the private sector was asked to invest, but JFC members were unable to obtain details of the bidding schedule in follow-on enquiries with government agencies.

70 HDM-4 provides a powerful system for road management, programming road works, estimating funding requirements, budget allocations, predicting road network performance, project appraisal, policy impact studies, and a wide range of special applications. Its development was sponsored by international funding institutions and supported by national governments, and other organizations, particularly: Department of International Development, UK; World Bank; Asian Development Bank; and the Swedish National Road Administration (www.hdmglobal.com/AboutHDM4.htm).

|

|

• Delayed submission of project requirements

Payment of claims by the government is subject to submission of complete supporting documents. In foreign-funded projects, submission of all required documentation must be completed within the loan period for the financial institution to release funding. When delayed, all payables are borne by the GRP. This imposes an additional burden to its limited budget.

• Delayed release of funds

A major cause of delayed implementation is the slow release of funds by DBM to implementing agencies.

Lack of Transparency in Procurement and Implementation

Transparency is a problem in almost all types of government infrastructure projects – whether JV, BOT, or government funded – and at all levels of government. Resources are misallocated. There were two large tollway projects where variation orders worth a few billion pesos were approved, and the public was not informed. Even the Congress in its oversight function has only very limited access to accurate information.

The Freedom of Access to Information Act (when enacted) will require disclosure of details of government transactions, such as infrastructure projects. It allows the public to request further information from the responsible government agency. In other countries, such as the US, there is a Federal Register where hundreds of government actions are published online for stakeholder input. If the government does not comply, its actions may be subject to post-hoc judicial challenge.

DPWH and DBM are already required to post on their websites information on major projects (e.g. the project amount, releases, expenditure, information of contractors and suppliers, etc.). But this is not followed in practice, especially for Congressional infrastructure projects. When agencies such as the DPWH and DBM are asked about non-disclosure of their projects, they respond that the information is “sensitive.” Information on suppliers and contractors is also not disclosed with government agencies explaining doing so would infringe on their “privacy.”

Lump sum and Congressional Allocations

Some projects cannot be specifically identified ahead of time; thus the justification for “lump sum” budgeting. Emergency projects such as typhoon and flood control and subsequent infrastructure repair and maintenance cannot be predicted exactly (although the country experiences typhoons and floods every year). Lump sums also include budgets for right-of-way and preliminary detailed engineering.

|

|

However, the largest amount of lump sums is classified under Various Infrastructure and Local Projects (VILP) where Congressional allocations are included. Legislators identify specific infrastructure projects for financing under this fund. The amount of lump sum in the 2009 DPWH budget was PhP 25 billion, out of a total capital program budget of PhP 86 billion.

Some projects are deliberately classified under the lump sum budget to make the spending non-transparent. Of the estimated CDF (PhP 70 million per congressman and PhP 200 million per senator), PhP 40 million is spent for hard or infrastructure projects (most of these come under the VILP of DPWH). There is no system that shows how and where money is spent. Sometimes money is spent on “ghost” or non-existent projects. Even within Congress, there is very limited transparency.

Cost overruns

Poor project preparation and implementation can lead to high cost overruns. A major source of additional and unforeseen costs is the non-cooperation of LGUs. In one case, a mayor threatened not to issue a permit for the LRT-1 north extension between Trinoma and Monumento if there would be no station in his city.

Risk sharing

Risk allocation must be defined at the beginning of a project in order to clarify the responsibilities of each party (public and private) in BOT, PPP, and JV projects.

|

|

Recommendations (25)

A. Double infrastructure spending to 5% of GDP with PPP. Overcome the constraint of low tax collection and the high budget deficit by harnessing available resources and capacities of the private sector for infrastructure development.

(Medium-term action)

B. Prepare, bid out, award, and implement with full transparency several large PPP projectsthat are already viable. This can create a pipeline of PPP projectsto attract domestic and foreign investors. (Immediate action NEDA, DOTC, DPWH, DOF, DTI, and private sector)

C. Potential pilot PPP projects include two rail and three toll road projects: LRT-1 South Extension and LRT-2 East Extension and the Cavite-Laguna Expressway, C-6, Expressway and SLEX 4 Calamba-Lucena. Total estimated cost of these five projects is PhP 173 billion. (Immediate action NEDA, DOTC, DPWH, and private sector)

D. To speed the process, use foreign technical and financial assistance; bring in experts who can be “embedded” in line agencies to prepare project bidding, evaluate proposals, and rank proponents with project monitoring to be done at PMS and final decisions made by the cabinet and the president. (Immediate action NEDA, DOTC, DPWH, and DOF)

|

|

E. Use available domestic capital for infrastructure investment. Interest rates are low and sustained growth in domestic liquidity indicates funds are available. Special Deposit Accounts and Reverse Repurchase Agreements total nearly PhP 1 trillion. (Immediate action private sector)

F. Create a coalitionof the Philippine Bankers Association, investment houses, and the Philippine Constructors Association and agree to promote good projects and good processes(transparent and competitive). Foster participation between local and foreign contractors, investors, and banks. (Immediate action private sector)

G. Amend the BOT Law. The role of the GRP in planning and preparing infrastructure projects for BOT should be more clearly defined. GRP should determine and identify projects it will undertake and projects to offer to the private sector under BOT/PPP. Increase Swiss challenge timeframe from 30 to 180 days. Pending passage of amendments, review again and issue revised BOT IRRs. (Immediate and medium-term action NEDA, DTI, Congress, and private sector)

H. Institute long range planning for infrastructure development. Plans should not be limited to one president’s six-year term of office. Infrastructure project planning should be depoliticized. NEDA should consider a 10-year plan, rather than encouraging plans, such as its MTDP and MTPIP, which are always for only a single presidential term. (Medium-term action NEDA, implementing agencies, and RDCs)

I. Government should minimize removing projects from its PPP priority list. All priority projects should be solicitedand awarded through public bidding. Require all major projects to undergo review by NEDA-ICC. (Immediate action NEDA and implementing agencies)

J. Study setting up a Philippine Infrastructure Facilitywith a World Bank (WB) loan, as Indonesia has done. Funds can be sought from donors, insurance companies, OFWs, and others. The fund could support project preparation and promote PPPs, as well as take equity and debt positions in projects. (Medium-term action NEDA and DOF)

K. Rescind or amend the EO on JVAs. Review all JV arrangements and ensure that they are consistent with NEDA Board policy that major projects (over PhP 500 million) should pass through the NEDA-ICC. (Immediate action NEDA and line agencies)

L. Require mandatory disclosure of projects under JVA prior to the signing of an agreement. Adhere to the principle “No decision is valid without pre-signing disclosure.” Review rules on risk sharing in the EO on JVAs. (Immediate action NEDA and line agencies)

M. Reduce cost overruns due to unsolicited inputs particularly from LGUs. Clarify the limits of LGU authority regarding national projects, but also include LGUs and local communities in stakeholder consultations to explain project benefits. Protect investors from political risks (TROs, LGU interference, right of way problems).(Medium-term action NEDA, DTI, DILG, LGUs, and line agencies)

|

|

N. Review foreign equity restrictions on infrastructurewith a view to maximizing foreign participation. (Immediate action NEDA, DTI, and DOJ)

O. Implement the National Transport Policy Frameworkand the National Transport Plan(2011-2016) that were prepared with the support of Australian Agency for International Development (AusAID). (Medium-term action NEDA and line agencies)

P. Build technical and legal capabilities of government agencies to prepare BOT projects, to have technical expertise to determine viability of BOT projects, to prepare feasibility studies, and to better allocate risks. More funding and technical assistance should be made available for such capacity building. (Medium-term action NEDA, DTI, line agencies, and private sector)

Q. Government should create reasonable timetables to address the long registration period of BOT projects. Upon submission of a proposal, there should be a 90-day deadline for approval. Information should be on agency websites with credible explanations when deadlines are not met. (Immediate action NEDA and DTI)

R. CDF should be utilized for necessary infrastructure projects and not follow political considerations. Strictly use HDM-4, which identifies and prioritizes project funding using objective technical and economic criteria. (Medium-term action DBM, DPWH)

S. Process and submit supporting documents during the loan periodprior to expiration of loan, so the financing agency shares payment of obligations. (Medium-term action NEDA, DBM, DPWH, and private sector)

T. DBM should release funds on timeto meet contractual obligations and diminish the backlog of payment obligations. (Medium-term action DBM)

U. Continue and strengthen the Pro-Performance Teamthat monitors infrastructure project implementation. (Immediate action OP and PMS)

V. Pass the Freedom of Access to Information Act. There should be a complete commitment to transparency. Create penalties for non-compliance of disclosure requirements and implement thoroughly. (Immediate action Congress)

W. Develop an on-line registry for information on infrastructure projects. Require permanent and updated online disclosure for priority projects, including timeline, status of project, proposed and actual expenditure, variation orders, etc. Foreign technical assistance should be requested to create a website to track major projects. When the Freedom of Access to Information Act is passed, it will be mandatory for government to fully disclose transactions. (Immediate action NEDA, DBM, and COA)

X. The private sector can also create a website tracking the top 200-300 large infrastructure projects, or find an independent government agency to create such a website (e.g. NEDA) without a need for legislation or an EO. (Immediate action private sector and NEDA)

|

|

Y. Lump sum budgets should be kept to a minimum, if not totally avoided, in order to promote transparency and accountability. (Immediate action DBM and DPWH)

Road and Rail FGD Participants, Moderator and Secretariat Members

November 12, 2009

Joint Foreign Chambers of the Philippines

FOCUS GROUP DISCUSSION ON ROADS AND RAIL71

___________________

71 The FGD on Road and Rail spent much of its time discussing reforms in process, resulting in the recommendations listed above. It also discussed roads and rails, and its recommendations for these are described under the Road and Rail section below. Its members included several former senior officials and investors with considerable experience in the Philippines who made valuable contributions.

|

|

Sector Background and Potential

With its archipelagic character, the Philippines depends on air and sea transport much more than countries with large continuous landmasses. Since a high percentage of domestic and international commerce and travel is by air and sea, the efficiency of aviation and maritime transportation has become increasingly critical to national competitiveness. There is much room to improve efficiencies and improve the logistics costs for goods and associated services. The high cost of domestic marine transport has long been questioned, while the enormous potential for tourism – both domestic and international – is greatly influenced by the quality of airports and seaports. Solutions to the numerous challenges involved in creating an efficient modern air and sea transportation system require addressing policy and regulatory impediments as well as upgrading and rationalizing airport and seaport infrastructure and networks.

Figure 68 shows the high rate of growth in passenger volumes for domestic air transport, tripling following the deregulation of the industry by former President Ramos in the early 1990s.

|

|

For several years (e.g. 1996-1997 and 2006-2007) annual increases were roughly 20%. Filipinos are flying more than ever, as competition in the aviation sector has provided affordable alternatives to maritime travel. More affordable air fares since the mid-1990s have also stimulated the growth of domestic tourism. Similar high rates of growth can be expected in the next few years, which will require more investment in modernizing airport infrastructure. Not only new terminals are needed. Few airports are equipped for night operations and most need navigational and radar improvements. Policies that encourage more direct international flights to secondary cities are urgently needed to relieve congestion at the Ninoy Aquino International Airport (NAIA).

Figure 69 shows the WEF ranking of air transport infrastructure for the ASEAN-6 with the Philippines ranked lowest, slightly lower than Vietnam and Indonesia and considerably lower than Malaysia, Singapore, and Thailand.

The Philippines lacks a modern showcase international gateway airport. Currently, the country has no airport even close to the quality of new facilities as regional competitors such as Bangkok, Beijing, Guangzhou, Hong Kong, Incheon, Kuala Lumpur, Nagoya, Narita, Osaka, Shanghai, Singapore, and Taipei. First impressions of foreign visitors arriving at the leading international gateways Manila, Cebu, and Clark are that terminal facilities are modest (NAIA Terminal 2 and Terminal 3 and Mactan), small, or dilapidated (Clark and NAIA Terminal 1 and domestic).

At NAIA, the airport master plan of the early 90s for three new terminals has not been followed. The cargo terminal has yet to be built, while new domestic Terminal 2 (T-2) and international Terminal 3 (T-3) terminals were built but have not been used for their original purposes. The new GOJ-financed domestic terminal that opened in 1999 has been used exclusively for domestic and international flights of Philippine Airlines (PAL) despite not being designed for requirements of international aviation (customs, immigration, and lounges).

|

|

The new international terminal, built by a Philippine-German joint venture, was expropriated by the GRP in 2004 when the owners were accused of corruption and overpricing. The two arbitration cases filed in the International Criminal Court in Singapore and International Centre for Settlement of Investment Disputes in Washington, have been decided in favor of the government in that the Anti-Dummy Law was violated. The DOF has given assurance that the government is committed to pay any amount the local Expropriation Court decides is due investors. Meanwhile, Cebu Pacific, the other major Philippine-owned airline, and Air Philippines and PAL Express have been allowed to relocate their NAIA flights from the ancient domestic terminal to T-3. International carriers, unwilling to move to T-3 until the ownership dispute is resolved, continue to operate from the very outdated Terminal 1 (T-1).

Full operation of T-3 will require the present taxiway to be closed so that only one runway will be available to all domestic, international, and general aviation flights. A fuel depot and lines must also be in place. Aside from T-3 being underutilized, the lengthy period since the government expropriation has created an irritant in RP-European relations and harmed the country’s investment image abroad. Expansion of NAIA beyond its current area of 600-hectares would require extensive demolition of business and residential areas.

The 1991 eruption of Mt. Pinatubo and subsequent erosion of Philippine political support for American military bases gave the GRP operational control of two extremely large installations at Clark and Subic in Central Luzon. Two decades later the special economic zones together host almost 145,000 employees and are becoming increasingly integrated, with Subic the international seaport and Clark the international airport serving the adjacent provinces.72 DMIA has room to build a 2nd and even a 3rd parallel runway adjacent to the two existing runways.

The Subic-Clark zone has tremendous potential for aircraft and ship assembly and maintenance, education, ITES, logistics, manufacturing, medical tourism, retirement, and tourism and could host many hundreds of thousands of more jobs with sound policies, promotion, and investment. Road connections from Manila to Clark and to Subic have greatly improved. In the decade ahead, the North Rail will become operational to San Fernando. A high-speed rail to link NAIA and DMIA has been proposed, and extension of rail service to Subic in the future should be considered, should the project be implemented (see Map 1).

Outside Central Luzon, airports in the various regions are being improved, although only a few have international service. Under the new National Tourism Act of 2009 (RA 9593), a province can be declared a Tourism Economic Zone, which could allow air or cruise ship service of any flag to operate with low taxes. Pocket open skies, which has stimulated tourism in several places in Asia, has not been tried in the Philippines, despite urging of such a policy for Clark from domestic business groups and foreign chambers.

However, the GRP negotiated bilateral air traffic rights agreements with 26 countries from May 2007 through February 2010, greatly expanding the potential number of flights between the Philippines and each country.73 These agreements are effectively bilateral open skies agreements since it will take many years to fully utilize the allowable inbound flights. Foreign airlines are burdened with the Common Carriers Tax (CCT) and Gross Philippine Billings (GPB), as well as customs, immigration and quarantine (CIQ) overtime charges, taxes and fees not imposed elsewhere and which make serving the Philippines less attractive for foreign airlines than more business-friendly regional destinations.

____________

72 Clark: 57,118 (2010) and Subic: 86,631(2010); total for freeports is 143,749.

73Australia, Bahrain, Brunei, Cambodia, Canada, Finland, Hong Kong, Iran, Japan, Kuwait, Libya, Macau, Malaysia, Netherlands, New Zealand, Oman, Qatar, Russia, South Korea, Singapore, Spain, Thailand, Turkey, United Arab Emirates, United Kingdom, and Yemen.

|

|

Map 1: High-speed rail connecting NAIA and DMIA

Foreign airlines and international courier delivery firms are currently considered public utilities and cannot serve the domestic market except as minority partners owning no more than 40% of equity. The two foreign courier delivery firms with hubs in the Philippines have shifted their hub flight operations from Clark and Subic to China to serve the latter’s fast-growing market.

|

|

Recommendations (15):

A. The GRP should prioritize investments in airport terminal, runway, and communication facilities. There is a need for an NCR/Central Luzon Transportation Master Planthat includes a strategy for development, until mid-century, of the major gateway airport(s) as well as minor airports. The plan should include ground rail and road transport infrastructure linking the airports and cities, including major ports. (Medium-term action DOTC and NEDA)

B. There should be only one international airport per region, with existing airports converted into international airports, in preference over building new airports. (Medium-term action by DOTC and NEDA)

C. Outside Central Luzon, priority should be given to Laguindinganin Northern Mindanao. At Mactan, the runway should be extended and high-speed ferry links to Tagbilaran increased rather than creating a new airport at Panglao. (Medium-term action DOTC and NEDA)

_____________

74 There is another view that NAIA should remain the primary international gateway since transferring to a less convenient airport may curb the growth of carrier services through a decrease in demand and an increase in operating expenses. There will be a market for regional, domestic, and general aviation services in Clark but not a full scale international gateway, even with a high speed rail connecting the airport to the CBDs in Metro Manila. Instead, NAIA should be expanded by expropriating land around the airport, be improved through major upgrades, and be optimized through better terminal allocation and efficient airport use management.

|

|

D. Make Clark an alternative gateway to Manila/NAIA.75 Eventually make Clark the primary international gatewayand NAIA the secondary, but still the primary domestic hub.76 Connect with a high-speed rail line(see Map 1). (Long-term action DOTC and NEDA)

E. The local Expropriation Court should quickly decide the amount due to NAIA T-3 investors. Subject to needed repairs and additional construction, begin to fully utilize the terminal for growing domestic traffic and for regional traffic using narrowbody aircraft. (If widebody aircraft are to use T-3, a new taxiway should be built separate form domestic runway 13-31.) (Immediate action DOT and DOJ with private sector)

F. Because T-1 is closest to international runway 06-24 and the international cargo terminals, T-1 should undergo phased renovationfor continued use by long-distance widebody aircraft. T-1 should eventually be connected to T-2 to allow domestic to international transfer between buildings.77 (Medium-term action DOTC)

G. A new fuel depot for NAIA is neededas the current depot leaks and is too close to T-1 and T-2. (Medium-term action DOTC)

H. If most international traffic is moved to Clark, there should be a second parallel runway, a terminal with a 20-million passenger capacity, and a high-speed railconnection.78 (Long-term action DOTC and private sector)

I. Quickly resolve the downgrading of the CAAPfrom Category 1 to Category 2 status by the US FAA and the 2010 EU decisionto prohibit Philippine carriers from European airports. (Immediate action DOTC and CAAP)

J. Improve the business and investment climate for international air carriers and enhance long-term connectivity, tourism, and trade competitiveness by setting the level of aviation taxes and charges to conform to international agreements and standards by removing discriminatory tax burdens such as the CCT and GPB.79 (Medium-term action DOF, DOT, and Congress)

_______________

75 NAIA has a land area of only 600 hectares, while DMIA has 2,367 hectares. NAIA is hemmed in by roads and dense commercial and residential development; Clark is not. NAIA cannot expand; Clark can.

76 NAIA handles 90% of the country’s international and 75% of domestic traffic. Manila Domestic Terminal is the oldest. Terminal 1 is the second oldest (1980s) and in an advanced stage of dilapidation. Over 20 foreign carriers use its 16 gates. Terminal 2 was opened in 1999. PAL, using 7 gates for domestic and 5 for international, has outgrown T-2. Terminal 3 has 20 gates but was built along the domestic runway which cannot handle wide-body aircraft.

NAIA runways are currently operating at full capacity from 7:00 am to 7:00 pm. Tourism is growing steadily, increasing the need for more international flights at Clark.

77 For T-1 and T-2 to connect, the fuel depot and NAIA cargo terminal must be relocated; the fuel depot at its current location is a hazard to both terminals.

78 Other Asian countries have relocated international gateway airports outside congested capital city airports. Hanoi, Hong Kong, Incheon, Jakarta, Kuala Lumpur, Nagoya, Shanghai, and Tokyo are examples. In some cases (such as in Nagoya and Tokyo) the older inner city airports have subsequently been allowed limited international flights. For residents of northern parts of the NCR, Clark is closer than Manila because of better highway connections to DMIA.

79 These tax burdens often exceed profit margins of international carriers and are not imposed in other regional countries. In the past decade Air Canada, Air France, British Airways, and United Airlines ended service to the Philippines, and Northwest Airlines dropped one of its daily wide-body flights.

|

|

K. Amend the Immigration Act of 1940, Tariff and Customs Code of the Philippines, and the IRRs of the Quarantine Act to relieve the burden from customs, immigration, and quarantine overtime, meal, and transportation charges for airlines and shippers. Declare 24/7 operations at all international airports and ports and make the State shoulder the overtime payments for CIQ personnel. (DOT, DOTC, DOF, DOJ, DOH, and Congress)

L. Revise take off and landing fees, make weight the main determinant, charge the same fees to international and domesticairlines.80 (Immediate action by DOTC)

M. Modify equity rules to allow Asian low-cost carriers to compete in the domestic market.81 (Medium-term action Congress)

N. Complete US$ 270 million GOJ-funded Communications, Navigation, and Surveillance/Air Traffic Management projectof the DOTC to modernize Philippine airports and improve air travel safety. (Medium-term action DOTC)

O. Make Palawan a Tourism Economic Zone, adopting pocket open skiessupported by infrastructure and a favorable tax regime (e.g. relief of taxes and fees such as GPB and CCT)82 (Medium-term action DOTC, DPWH, DOF, DOT, Congress, and LGU).

Airports and Seaports FGD Participants, Moderator and Secretariat Members

November 26, 2009

Joint Foreign Chambers of the Philippines

FOCUS GROUP DISCUSSION ON AIRPORTS AND SEAPORTS

______________

80 International airlines pay double the take off and landing fees charged to domestic airlines even for the same aircraft types, in effect subsidizing the domestic carriers.

81 ASEAN is moving towards complete open skies and may someday adopt unrestricted ownership of airlines operating within ASEAN. Indonesia, Malaysia, and Vietnam permit up to 49% foreign ownership of an airline. Most bilateral air service agreements (ASAs) specify that beneficiary national airlines have substantial if not majority local ownership.

82 Successful pocket open skies examples in Asia include Hainan province in China, Kota Kinabalu in Malaysia, and Siam Reap in Cambodia. In 2009, each received 750,000, 562,000, and 2.2 million international visitors, respectively.

|

|

Sector Background and Potential

Electric power and water are essential needs for modern man, to survive, and to thrive. In the globe’s fastest-growing region – Asia – they are especially critical to economic growth and competitiveness.

The Philippines is approaching the end of a two-decade transition from a public sector power generation monopoly to a private-sector-led “open access” competitive environment with enhanced government regulatory oversight. Yet its electricity prices remain among the highest in Asia, and supply shortages are present today in the Mindanao and Visayas grids and are possible in two years in the Luzon grid. Unreliable and expensive electric power is a serious deterrent to foreign investment.

The main objectives of the open access policy in the Electric Power Industry Reform Act (EPIRA) that became effective in mid-2001 are (1) to build a sustainable and reliable power supply and (2) to lower electricity rates in the long run. To encourage new investment in power supply, electricity rates have to go up in the short-run (reflecting both the limited supply of power generation capacity and the need to dispatch oil-fired plants to meet the demand). Rates will go down only when new and more efficient generating plants are commissioned that are profitable at a much lower cost per kilowatt-hour, such as coal-fired plants, thereby creating an abundant and more competitive supply of power and minimizing the dispatch of oil-fired plants.

The conditions precedent to open access will have been met by year-end 2010: (1) the unbundling of generation, transmission, and distribution; (2) elimination of subsidies; (3) initiation of the Wholesale Electricity Spot Market (WESM); (4) privatization of at least 70% of the power plants owned and operated by the GRP; and (5) transfer of management and control of at least 70% of the contracts between Independent Power Producers (IPPs) and National Power Corporation (NPC) to IPP administrators. Conditions 4 and 5 were only met recently. The Energy Regulatory Commission (ERC) is expected to declare open access no later than 2011.83

_________________

83 As of April 2010, 3,318 MW representing 88% of the government-owned generation plants had been sold yielding $3.47 billion which has been used to pay down NPC’s debt. National Transmission Corporation (TransCo) was privatized to a China-Philippine operating concessionaire in 2008.

|

|

Eventually, open access should encourage more competition in the supply of electricity and lead to lower electricity prices. Electricity prices in the Philippines are the most expensive in Asia and harm competitiveness. Figures 70 and 71 show the cost of residential and industrial electricity in the Philippines and six other Asian economies.

Figure 70: Residential retail electricity tariffs, selected Asian economies, USc/KWh, 2010

Figure 71: Industrial electricity tariffs, selected Asian economies, USc/KWh, 2010

Figure 72 shows the percentages of installed generating capacity by type of power source. Hydrocarbon fuels (coal, gas, and diesel/oil) comprise 66% of the total. Figure 73 shows the percentage of the actual generation that comes from different fuel sources. Comparing Figure 72 to Figure 73 shows that the more expensive and more polluting diesel/oil capacity is not being dispatched by power regulators.

|

|

Renewable energy sources (geothermal and hydro) constitute 33.6% of generation capacity and 32.5% of the power mix. Unlike Indonesia, the Philippines does not have large unutilized geothermal fields to develop. A Renewable Energy Act of 2008 (RA 9513) was passed in 2009 providing generous fiscal incentives to investors. When the feed-in-tariff (FIT) is announced some of the many potential projects licensed in the past year with the DOE may begin to become real power generators.84

The current Administration could be the first to experience the positive effects of the EPIRA, i.e. a reliable supply of less expensive power. The policy it follows in this new environment will be critical to the success of open access. Unfortunately, as of early 2010, a serious policy deficiency exists. Without a clear energy policy that indicates where the country should source future energy requirements, taking into account its current power situation and what it is prepared to spend (affordability) and/or guarantee (such as credit enhancements), there will be underinvestment in power. Only through a well-conceived master plan will investors know the areas in which they can invest with reasonable certainty.

___________

84 Feed-in tariff is the minimum price distribution utilities are required to pay, which will be passed on to consumers as a renewable energy (RE) charge. The FIT is required for RE power plants – because of their higher construction costs than conventional plants using hydrocarbon fuels – in order to assure that investors receive a reasonable return on their investments.

|

|

There is a limited supply of power in the Philippines (see Table 33). Thailand has 40,669 MW power capacity serving 67 million people. South Korea has 79,859 MW serving 49 million. The Philippines has only 15,680 MW (and not all is considered reliable) for 90.3 million people. Electricity consumption per capita in 2008 in the Philippines (588 KWh) was close to Indonesia (591) and Vietnam (799) but much less than Malaysia (3,506), Singapore (8,185), and Thailand (2,079).

|

|

• Luzon

The power situation in the Luzon grid has been relatively stable since the late 1990s. As of late 2009, there is a surplus in generation due to a slowdown in demand growth brought about by the global financial crisis. Yet there was still positive growth in kilowatt-hour sales during the entire year. According to the WESM, peak demand in Luzon grew 5.2% year-on-year reaching 6,886 MW. On a good day in late 2009, the power supply to the Luzon grid was only about 8,000 MW (15-20% of which came from oil), falling below the statutory reserve margin. Under open access, there are 5 to 6 generators in Luzon that have capacity that is not locked up or sold under contract, 55 distribution utilities, and 1,500 contestable customers. Having 5 to 6 generators with only 1,500 customers is not balanced.

The coal-fired GNPower 600 MW plant in Mariveles, Bataan, began civil works in early 2010 and is expected to become operational in late 2012 or early 2013. Other additional capacity is expected from the rehabilitation and expansion of the privatized NPC hydropower facilities. The construction of additional baseload plants is essential to provide adequate reserve and to avoid power blackouts. With piers, designated sites, and Environmental Compliance Certificates (ECCs) in place, Ilijan, Pagbilao, and Quezon Power plant expansions can be brought into operation considerably faster than new greenfield plants.

Figure 75: Power demand and supply outlook, Luzon, in MW

Figure 76: Required reserve margin and peak demand estimates, Luzon, in MW

|

|

• Visayas

The Visayas grid suffers from long-standing problems in power supply. However, ongoing construction of coal-fired power plants scheduled to come on line in 2010 and 2011 will ease the supply shortage problem by adding some 600 MWs to the grid. Cebu Energy Development Corporation has constructed two of the three new 82 MW coal-fired power units in Toledo, Cebu, the third of which is expected to be commissioned in early 2011.85 Two of the partners in the same firm are constructing a 164 MW coal-fired plant in the Panay sub-grid in Iloilo City for completion in 2011. Another on-going development for the Cebu sub-grid is the 200 MW KEPCO-Salcon plant in Naga City to be operational in 2011.

Figure 77: Power demand and supply outlook, Visayas, in MW

Figure 78: Required reserve margin and peak demand estimates, Visayas, in MW

• Mindanao

Mindanao also has been plagued with power supply problems and transmission constraints. The latter are being addressed by the new transmission concessionaire, National Grid Corporation of the Philippines (NGCP). Too few generating projects are under construction in Mindanao, including the Sibulan hydropower project of HEDCOR Inc to serve the Davao Light & Power Company and the Conal Holdings Corporation (2 x 100 MW) coal-fired plant in Maasim, Sarangani.

____________

85 Since its groundbreaking on January 26, 2008, the first of the three 82 MW units was switched on March 5, 2010. The plant’s second unit has been providing power to the grid since May 21 (Global Business Power Corporation website: www.gbpc.com.ph).

|

|

Figure 79: Power demand and supply outlook, Mindanao, in MW

Figure 80: Required reserve margin and peak demand estimates, Mindanao, in MW

Table 34: Expected new sources of electric power

|

|

The Philippines should have an overabundance of supply for competition to work in lowering electricity prices. Is it realistic to expect that the new power capacity shown in Table 34 will be constructed in the near future (next five years)? Is it realistic to expect international financing absent take-or-pay contracts/guarantees?

It is difficult to find investors to construct a merchant plant. There is a very limited pool of deep-pocketed local investors who have made the effort to learn the Philippine energy market (e.g. Aboitiz, Ayala, First Gen, Metro Pacific, San Miguel, and SM) and limitations apply to foreign investment (e.g. the 40% minority public utilities and natural resources equity provision) for some forms of traditional and renewable energy projects. The poor reputation of Philippine courts and legal processes with respect to enforcing contract provisions on a timely basis further discourage investors.

Financial institutions conduct extensive due diligence investigations and do rigorous research to finance both merchant plants and those supported by off-take agreements. Banks look at creditworthiness (historical reliability in payment and sufficient cash reserves) and the ability of proposed power plants to produce reliable revenue and cash flows. In 2009 global credit markets shifted to short-term (5-7 year) financing. However, power plants require long tenors to make a project viable. Long-term (10-15 year) financing for generating projects with off-take agreements for a substantial percentage of their capacity is a challenge and becomes impossible if the merchant portion becomes too large.

Multilateral financial institutions such as the International Finance Corporation (IFC) and the ADB have been willing to finance merchant power plants under certain circumstances, if the technology is proven and operating risks are identified and mitigated. Both institutions emphasize climate change issues, making it difficult for them to finance coal-fired power plants. However, ADB is participating in financing the new coal-fired power plant in Naga, Cebu in light of the power crisis affecting the Visayas grid. At the same time, the ADB and the IFC are undertaking measures that would offset this decision, such as encouraging the development of renewable energy. The ADB is in discussions with the DOE to create a Clean Technology Investment Plan.

The creditworthiness of electric cooperatives as buyers of power is important for merchant plants for off-take. Cooperatives are being forced to be more disciplined in fulfilling their payment obligations now that Power Sector Assets and Liabilities Management (PSALM) has privatized much of the government-owned capacity serving the Luzon and Visayas grids. In their previous dealings with NPC, some cooperatives lagged behind in payments. Now dealing with the private sector, they risk being cut off if they do not pay their bills. Electric cooperatives face several challenges: (1) institutional preparedness to participate in WESM, (2) financial capacity or creditworthiness, and (3) technical capacity for power planning and maintenance.

Coal is a relatively inexpensive, plentiful, and reliable source of energy. If Europe, the US and other environmentally conscious countries still rely on coal to fuel their generating plants, then the Philippines should also be using coal to supply power to consumers. The main criticism of coal is it that is bad for the environment. To mitigate this, the Philippines can take advantage of its geography by choosing a small island that is not in close proximity with populous areas and make it a coal-fired power-generating island. For example, Semirara is an island with coal deposits and has very few inhabitants, making it easier to relocate affected families.

|

|

Contrary to public expectations, the Philippines does not have extremely high potential RE resources (hydro, geothermal, wind, solar, and biomass). The maximum capacity that can economically be extracted from RE sources may only be around 3,000 MW. The country has numerous run-of-river small hydro sites, but has limited undeveloped large hydro sites with seasonal storage capacity and has limited major undeveloped geothermal resources.86 Renewable energy is not sufficient to address the energy needs of the Philippines. Restrictions on foreign equity in the RA 9513 IRRs – which are not specified in the law itself – that limit foreign ownership to 40% will discourage foreign participation and slow the development of RE projects, except for geothermal which falls into a separate category.

Table 35 shows estimated gigawatt capacity for biomass, geothermal, hydro, and wind for five Asian countries. While the Philippines already has significant current geothermal and hydro capacity and more potential to develop both resources, as well as biomass and wind, the potential resources are not sufficient to meet the country’s future generation requirements economically.

Table 35: GW power capacity of renewable energy resources, selected East Asian countries, thousand MW

Liquefied natural gas (LNG) is a viable power fuel solution for the Philippines. The LNG trade in SEA is a very large business – with Japan, South Korea, and China as the largest markets. The Philippines is close to the major LNG exporters (Papua New Guinea, Australia, and Brunei) whose tankers can pass by the Philippines. However, LNG requires a major investment in infrastructure – much more than any single power plant of a capacity suitable for the Luzon, Visayas, or Mindanao grids. No investor or lender is willing to risk a major investment in the billions of dollars without reasonable assurances of a stable investment climate and sufficient volume to support it.

The San Miguel purchase of the 620 MW Limay, Bataan combined-cycle gas-turbine asset offers the potential for LNG in the Philippines, provided other customers can be found (power, industrial, commercial, and institutional). Hundreds of millions of dollars are needed to create the initial plant, but the opportunities for gas are immense. The Dominican Republic originally started LNG in a power station, then it was extended to transportation, to other power stations, and to generation facilities burning heavy fuel. The country now has the most diverse fuel mix in the Caribbean/Central American region, generating high savings (US$ 160+ million after 3-4 years). To replicate this, the Philippines has to have clear policies to attract investment in LNG.

_____________

86 In contrast, many undeveloped geothermal fields in Indonesia have capacities of 300 MW or more, while in the Philippines they mostly range from 30 to 50 MW. Indonesia, with potential for 22,000 MW of geothermal power, recently received a large World Bank loan to develop RE energy.

|

|

Retail power prices in the Philippines are among the highest in the Asia-Pacific region. How can the Philippines lower its power rates? Tariffs will not go down immediately after the declaration of open access because spot market prices must exceed the marginal cost of a new plant to encourage more investment in supply.

As of November 2009, the price of electricity at the WESM typically is PhP 2 per KWh, while the long range marginal cost of a new plant is about PhP 4 per KWh. Based on market studies, electricity rates in Luzon will not cross the long range marginal cost of a new plant until 2013 or 2014. Hence, there is minimal incentive to commit to building a new plant unless much of the infrastructure is already in place. When this happens two expansions may be the first to be financed and constructed: the Quezon coal-fired plant where additional capacity of 300-500 MW can be created by adding an additional unit using the same common facilities and, similarly, the Pagbilao coal-fired asset (also in Quezon province), where a third unit of 350 MW can be added.

Hydropower projects that were designed for capacity additions include the CBK pumped storage asset, with provisions for additional units 5 and 6 for about 350 MW; the Pantabangan hydro asset with provisions for another 112 MW; and the Magat hydro asset with provisions for an extra 180 MW. On the other hand, the development of the 600-MW coal-fired project of GNPower in Mariveles, Bataan is well advanced after its project financing closed in early 2010.

From the point of view of lender participants in power generation project financing, the main requirement is sustainable cash flows to cover debt service. A power generation project must have sufficient and reliable revenues from bilateral power supply agreements and spot market sales to make debt service payments and yield a return to its equity participants. Tariffs can decrease after the loans are repaid.

|

|

In the long run, nuclear technology offers the greatest prospect for cheaper power. But this option has been opposed by public concerns for the risk of accidents and the disposition of the wastes. However, experience around the world shows there are very few accidents. Furthermore, the technology for waste disposal is available and is only a small portion of overall operation costs. Both Japan and Taiwan have many nuclear plants and are considering building more. South Korea has 21 nuclear power plants serving 35 million people that account for 50,000 MW. Four more nuclear plants currently are under construction with two more planned within the next five years. China has nuclear plants and is building more in order to almost double its nuclear power capacity to 70 GW by 2020. Malaysia, Thailand, and Vietnam also have decided to introduce nuclear power in the next decade (see Table 36).

Table 36: Nuclear plants under construction, selected economies, 2009

KEPCO was scheduled to submit a feasibility study to NPC at the end of 2009 to determine whether the Bataan nuclear power plant can be rehabilitated. Nuclear is a viable source of power supply for the Philippines, but not for at least 10 years. The smallest viable capacity for a nuclear power plant is 1,000 MW. At this time, the Luzon grid can only accommodate a maximum unit size of about 600 MW. The Bataan nuclear power plant would have operated at only 400 MW had it commenced operations in 1985. Measures were introduced in the 14th Congress to encourage operation of the Bataan Nuclear Power Plant.

Experts estimate that at least 15-25% of the consumption of electricity is wasted. Wastage can be mitigated significantly by reducing the system losses of distribution utilities and the national grid, including losses due to theft, as well as by implementing a wealth of energy efficiency and conservation measures. These can save most consumers 10-15%, yet recover associated costs within one to three years. The DOE is preparing to introduce an energy efficiency bill in the 15th Congress that will encourage and provide incentives for such measures. There are also ODA programs available to assist the Philippines to become more energy efficient. The IFC is working with local banks via a Sustainable Energy Finance Program to provide relevant technical knowledge to lend to energy efficiency and renewable energy projects. The IFC hopes to create energy savings by encouraging demand side conservation at private sector facilities such as factories, large offices, and malls.

Insufficient power transmission capacity (the transmission line transformers, reactors, and capacitors) affects system reliability, security, and stability. The Grid should remain stable after any Single Outage Contingency and should also remain controllable after a Multiple Outage Contingency. There are instances when the outage of a single transmission line or transformer causes power interruptions or deloading of generators. Insufficient power transmission capacity forces generators to be constrained-off and unable to deliver full power because of limited capacity. This situation could allow a more “expensive” generator to be dispatched in favor of a “cheaper” generator, in effect increasing WESM prices. NGCP needs to ensure sufficient transmission capacity at all times, anticipating the load growth in each grid, to adequately serve Generation Companies, Distribution Utilities, and Suppliers requiring transmission service and ancillary services.

|

|

|

|

Recommendations (21)

A. Ensure that EPIRA targets for open access are achieved and declare open access on schedule before the end of 2010.87 The ERC should promulgate the necessary and appropriate Rules and Regulations in a timely manner. (Immediate action DOE, PSALM, and ERC)

B. PSALM should solicit and award bids from the private sector for the Agus and Pulangi hydro facilities during 2010 so that ownership can be transferred in June 2011 as currently authorized by EPIRA.88 (Immediate action DOE and PSALM)

C. Formulate an integrated energy policy and master plan giving clear direction for sources of energy, locations of power plants, capacityeach source generates (accounting for future demand), transmission of energy supply, policies to attract large investors and lenders (into LNG, nuclear, coal, renewable energy, and others) and importation of energy. The master plan must take into account the threats and/or challenges of climate change, energy efficiency, and availability of new technology. The priority power sources (biomass, coal, gas, geothermal, hydro, LNG, nuclear, wind, and others) should be strategically located throughout the country taking into account maximum capacity of each source. (Immediate action DOE, NEDA, and private sector)

D. The National Renewable Energy Board should create a roadmapto complement the overall energy master plan of the DOE recommended above. (DOE with private sector)

E. The weak creditworthiness of most distribution utilities and electric cooperatives likely requires some form of credit enhancement to support project financing and power supply agreements of new generating projects withoff-take agreements with such parties. Revisit policy disallowing “take-or-pay” or sovereign guarantees, in light of what makes economic sense. (Immediate action DOE and DOF)

F. Strongly encourage industrial, commercial and institutional load customers, distribution utilities, and electric cooperatives to establish their creditworthiness. (Immediate action DOE, DOF, and private sector)

G. Remove all foreign equity restrictions for power projectsto create a level playing field and attract more foreign energy players to invest.89 (Medium-term action NEDA and DOE)

____________

87 PSALM achieved privatization of 83.3% of NPC generation assets and 34% of the IPP administrator contracts as of November 2009. The target is to declare open access before the end of 2010.

88 The hydro generation facilities in Lanao del Norte and Bukidnon provinces were excluded from privatization for a decade when EPIRA was enacted in 2001. The El Niñ¯ ¥xperience during late 2009 and 2010 has clearly tested the capacity of these plants. They are excellent assets that will be better managed, maintained and expanded by the private sector, as evidence by hydro generating assets already privatized within the Luzon grid.

89 Restrictions on foreign capital placed in the IRRs of the Renewable Energy Act will limit the pace of development of RE power, contrary to the apparent intent of the law, which contains no such provision. Interpretations that dams cannot be foreign-owned, but turbines within them can, should also be re-examined with a view to promoting needed investment.

|

|

H. Ensure that contracts are strictly enforced. Rules and regulations must not changein the middle of project implementation or be reinterpreted retroactively. (Immediate action DOJ and DOE)

I. Partners such as ADB, IFC, and JBIC can help finance the longer tenor– the “tail risk” beyond 10-12 years – when international private banks are only comfortable with shorter tenor. (Immediate action ADB, IFC, JBIC, and private sector)

J. The RP must find ways to comply with the requirements of lending institutions in dealing with climate change issues. Create the Clean Technology Investment Planand implement thoroughly. (Medium-term action DOE, ADB, and private sector)

K. The DOE needs to implement a policy with assistance from the private sector to assist cooperatives in the transition to a privatized electric power industry. Power generation companies should be interested in the creditworthiness of their clients. Strongly encourage electric cooperatives to establish their creditworthiness. (Immediate action DOE, NEDA, and private sector)

L. Develop a power plant on an isolated island such as Semirarawith a supply of indigenous coal and deepwater access to international coal sources. Connect the island to a grid via submarine cables, for example to Mindoro and to Batangas. This will close the loop of Bicol, Samar, Leyte, Cebu, Negros, Panay, Boracay, Semirara, Mindoro, and Batangas. (Long-term action DOE, NGCP, and private sector)

M. Study the potential of LNGin the Philippines and create a comprehensive policy to attract investment in this sub-sector. LNG can be a greener alternative sourceof energy. Converting public transportation to LNG will generate large savings, have less negative effects on health, and reduce traffic congestion. (Medium-term action DOE and private sector)

N. Merchant plants cannot succeed without a mature spot market to establish the correct price. Investment will not occur in this market if the price is below the long-range marginal cost of a new plant or at or less than the variable cost of plant operations, including fuel. (Immediate action DOE and WESM)

O. Implement open access. EPIRA requires removal of cost subsidies to reflect the true cost of electricity. Over the short term, electricity prices are likely to increase. The only way to bring the price down is for new generators to enter the market with plants that are profitable at a much lower cost per kilowatt-hour, thereby creating an abundant supply of baseload, intermediate, and peaking capacity. This can happen only via open access.

P. The RP should include the development of nuclear power in the national power development plan. Preparations needed for this technology require at least 10 years, and infrastructure, power plant, and transmission require very large investments. The Philippines should come to a decision soon and then strategically prepare for the next 10 years. (Medium-term action DOE)

|

|

Q. Congress should pass a resolution supporting consideration of the development of nuclear energy, including small-scale nuclear power options currently under development, while leaving disposition of the Bataan Nuclear Power Plant for the Executive to decide. (Immediate action DOE and Congress)

R. Congress should pass an Energy Efficiency Actafter full consultation with stakeholders. The RP should implement foreign donor and national projects to improve energy efficiency. Efforts of distribution utilities to reduce system lossesdue to theft must be strongly supported. Capital investment in the transmission and distribution systems to reduce systems losses should be incentivized. (Medium-term action DOE, Congress, and private sector)

S. Explore the possibility of WESM sales of freely-tradable forward power supply contractsin relatively small denominations (such as 5 or 10 MW) and applicable for specified timeframes (e.g. short, long, baseload, and peaking) for sale to load customers or investors. Investigate performance security options to protect parties to such forward contracts. (Medium-term action DOE, WESM, and private sector)

T. Interconnect the entire grid to enable producers to transport electricity to other parts of the country via the WESM. With a truly national grid, investors will be able to come in and take advantage of the growing demand for power supply. There must be an abundance of supply for the WESM to be effective in lowering costs of electricity. (Medium-term action DOE, WESM, and NGCP)

U. NGCP and the ERC should accelerate capital investments to resolve constraints limiting the flow of powerfrom Luzon to the Visayas and from southern Luzon to the NCR and from northern Luzon to Metro Manila. NGCP should continuously evaluate the technical and commercial feasibility of interconnecting the Luzon and Visayas grids via submarine cable with the Mindanao gridand/or various isolated grids, such as Mindoro. (Medium-term action NGCP, ERC, and DOE)

Power and Water FGD Participants, Moderator and Secretariat Members

November 17, 2009

Joint Foreign Chambers of the Philippines

FOCUS GROUP DISCUSSION ON POWER AND WATER

|

|

Sector Background and Potential

Ground transportation infrastructure is essential for investment and job creation which are necessary to reduce poverty in the Philippines. It is a “catalyst” for area development and economic growth. Transport-logistics infrastructure such as roads and rail facilitate the efficient movement of goods and people. Absence of such vital infrastructure impedes the efficient movement of goods, increases transport cost, and ultimately impacts negatively on the country’s competitiveness.

Modern roads and rail support the high-growth sectors of BPO, manufacturing, and tourism. Modern toll roads and better farm-to-market roads provide tourists better access to destinations. In large urban areas particularly Manila a more extensive light rail system moves both employees and tourists more efficiently and eases traffic congestion on major thoroughfares.

The government allocated roughly PhP 889 billion to the development of transport infrastructure (roads, rail, light rails, airports, and seaports) under the 2006-2010 Medium Term Public Investment Program (MTPIP). For 2009, DPWH’s budget reached almost PhP 130 billion, the largest amount in the national budget and the highest level ever for the department (see Figure 82). The DPWH builds roads and bridges, school houses, and other public works. However, Figure 81 suggests that this increased spending has not raised the overall quality of roads.

|

|

One reason for the continued low rating of roads may be that much of the increased DPWH spending is going into CDF roads that are usually barangay roads (see Figure 83). As a result, national roads have barely increased in the last two decades. However, traffic on national roads certainly has. Anyone stuck for hours on EDSA or who tries to navigate the old MacArthur Highway north of Manila or the pre-SLEX road passing through the Laguna hometown of national hero Dr. Jose Rizal knows government funds are not improving these roads.

Figure 83: Total road length (km) development, 1982-2007

National roads are needed for efficient interprovincial movement of goods and people. One reason Philippine intercity traffic is becoming more congested is that the Philippines has not been adding to its stock of national roads for many years (see Figure 84).

Figure 84: Length of national/state roads, in ‘000 km

|

|